The market premium for MicroStrategy’s Bitcoin holdings has narrowed to near parity, raising questions about the future of Michael Saylor’s leveraged Bitcoin model.

According to the latest disclosure, the company owns 649,870 BTC at a cost of approximately $48.4 billion, but its shares are no longer trading at the high multiples that supported its previous expansion.

Collapsing premiums and rising capital pressures

The company’s mNAV fell below 1x in November. mNAV (market-to-net asset value) measures how much more (or less) an investor is willing to pay over the value of the strategy’s underlying asset, Bitcoin.

Sponsored Sponsored

This is important because Strategy’s entire accumulation strategy relies on issuing shares at a premium. This means that every time a new share is sold, existing holders receive more Bitcoin per share.

This sharp reversal in mNAV comes on the heels of a broader market downturn. Bitcoin has fallen more than 30% from its October high to below $90,000.

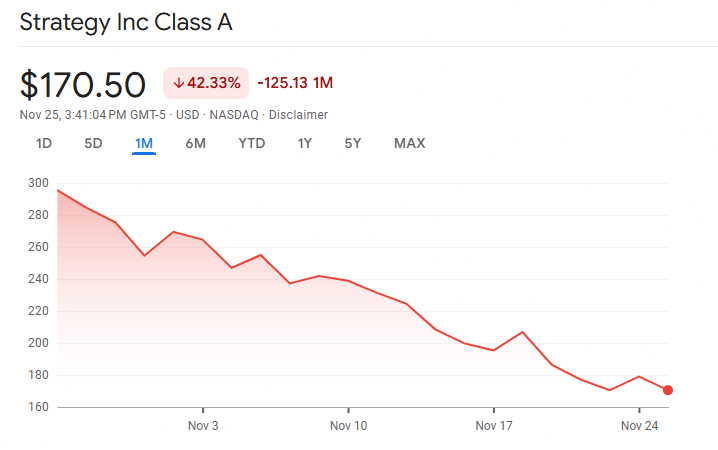

Meanwhile, the decline in Strategy shares accelerated, reflecting concerns about the company’s reliance on capital markets and rising preferred stock costs.

The capital structure of the strategy is a central issue. The company has only $54 million in cash and owes more than $640 million in annual preferred dividends.

The company’s software business will continue to have negative cash flow in 2025, and the gap between debt and internal liquidity is widening.

As a result, strategies have become dependent on capital markets. The company raised about $20 billion in the first nine months of 2025 through convertible debt, preferred stock and market equity.

This fund continued to accumulate Bitcoin while offering high and rising coupons on older items.

Sponsored Sponsored

However, the mechanisms that once fueled this model’s growth have weakened. At a time when Strategy Inc. was trading at a significant premium to net asset value, the stock issuance increased Bitcoin per share for holders.

That effect disappears when the premium collapses. Issuing shares close to NAV risks dilution rather than accretion.

As the cost of capital rose, so did the pressure. The company’s STRC preferred stock raised its dividend to 10.5% in November from 9% in July to maintain par value.

The new priority service includes a coupon of more than 10%, with penalties of up to 18% if unpaid. These conditions increase annual costs and increase investors’ concerns about sustainability.

Market liquidity, MSCI risk and the future of premiums

After the October 10 crash, market confidence further deteriorated. Bitcoin fell about 17% as leveraged liquidations exceeded $19 billion. Order book depth collapsed across exchanges, highlighting the vulnerability of liquidity during times of stress.

Sponsored Sponsored

For him, who owns more than 3% of the bitcoin supply, the episode has heightened concerns about a possible forced sale.

The threat of index inclusion makes the problem even worse. MSCI is discussing removing companies from its index that hold more than 50% of their assets in digital currencies.

Strategy ranks close to 77% of Bitcoin in terms of asset share. JPMorgan estimates that these exclusions could lead to negative outflows of about $2.8 billion, which could reach up to $8.8 billion if other index providers follow suit.

MicroStrategy’s mNAV may be further compressed if index delisting moves forward in February 2026. Lower premiums reduce the viability of equity issuances that Strategic has used to manage its debt and continue accruing.

Continued discounts will complicate refinancing and weaken the company’s ability to protect its capital structure.

Sponsored Sponsored

Strategy claims its balance sheet provides long-term strength. The company recently claimed that it would guarantee dividends for “71 years” based on Bitcoin’s current market value.

However, this calculation assumes smooth sales, no price impact, and no tax liability. The October crash demonstrated how quickly liquidity can evaporate under stress.

Will MicroStrategy’s Bitcoin Premium be revived?

The reduction in mNAV reflects a reassessment of market leverage, liquidity and risk. Investors appear less willing to pay a premium for the exposure they can access through spot Bitcoin ETFs without a corporate bond or preferred stock layer.

The premium could return if Bitcoin rises sharply or if index providers soften their stance. However, structural pressures remain.

Higher dividend obligations, negative operating cash flows, and lower equity premiums make the strategy more risky than before.

Until these pressures ease, the market message is clear: Investors no longer pay extra for strategic models, and the days of easy issuance seem to be over.

Premium returns now depend on the strength of Bitcoin, index decisions, and the strategy’s ability to survive the most difficult period in history.